Introduction

A great company is not always a great stock. Company quality is judged through competitive strength, cash generation, market position, and durability. Stock attractiveness depends on those things too, but it also depends on expectations, price location, positioning, and valuation.

That difference matters more than most beginners realize. When people mix up company quality and stock attractiveness, business analysis turns into story-telling and investing turns into vague optimism.

Why business structure matters

The first useful question in investing is not “Is this company good?” but “What exactly am I evaluating?” A great company and a great stock are related, but they are not the same question.

A great company usually has durable advantages, solid cash generation, and a business model that can absorb shocks. A great stock is a company whose quality is not already overpaid for by the market.

Core framework

A great company usually shows three things. First, it has some real competitive edge in product quality, customer relationships, brand, regulation, or switching costs. Second, it converts business success into real cash flow. Third, it can stay durable even when the cycle gets tougher.

A great stock is different. You have to ask how much of that quality is already priced in, whether expectations are stretched, and whether the current price leaves room for positive surprise. A great business can still be a weak stock if the market already expects too much.

That is why these two ideas often separate. A clearly superior business can become a difficult stock when expectations are too rich. A less impressive business can become a strong stock for a while if expectations were far too low and the structure starts improving.

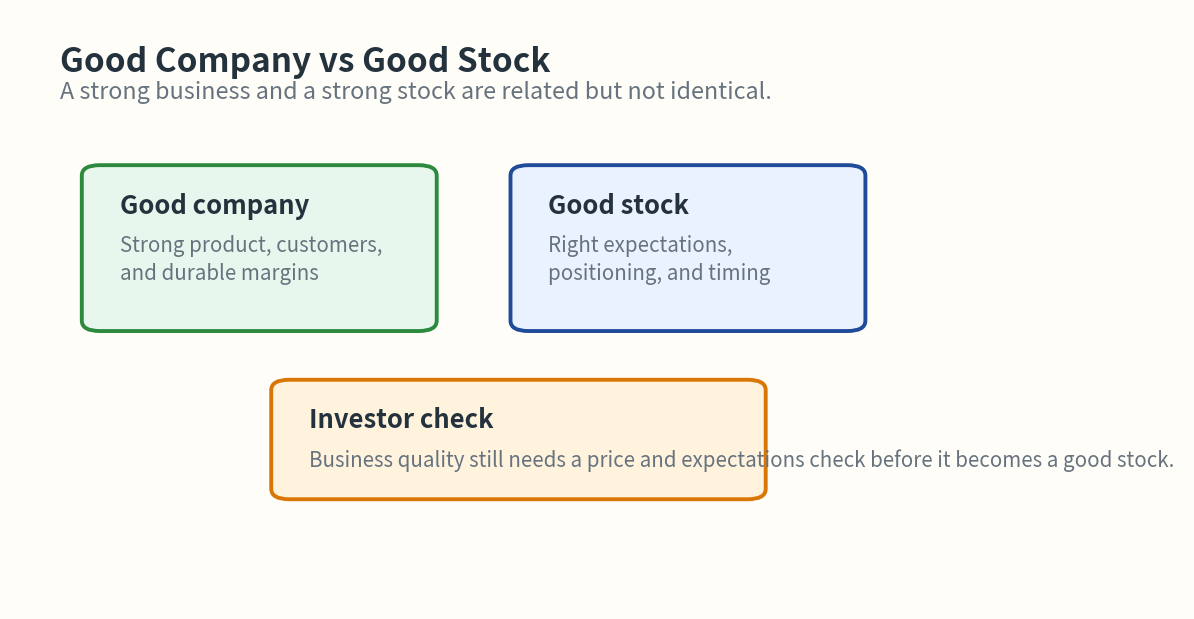

Visual guide

Business quality and stock attractiveness are not the same axis. Separating them reduces false confidence.

Where to verify it

This question becomes clearer when you read company documents and market behavior together.

- In the annual report, start with business description, risk factors, financial statements, and investment or contract disclosures.

- In recent disclosures, check contracts, investment, financing, buybacks, dividends, and earnings updates.

- In financials, look beyond revenue growth and focus on operating margin, operating cash flow, leverage, and return on equity.

- On the price side, check where the stock was trading before the event, how large turnover was, how it closed on the day, and whether the move held over the next few sessions.

The key is not to mix the evidence for a great company with the evidence for a great stock in the same note.

What to check in a company

The most practical sequence is this:

- Write down where the company actually makes money.

- Check whether that structure is repeatable and defensible.

- Confirm through disclosures and financials that the business is still holding up.

- Only then ask whether expectations and price location still leave room for upside.

Investor checklist

- Did you separate the evidence for company quality from the evidence for stock attractiveness?

- Can the business advantage be confirmed in filings rather than only in management language?

- Is the current price already reflecting very high expectations?

- Did you avoid skipping valuation and positioning just because the company looks strong?

Typical misunderstandings

- If the company is great, the stock must automatically be attractive.

- If the stock performed well, the company must be great.

- Business quality and stock quality can be merged into one simple conclusion.

Example scenario

Imagine an industry leader with strong market share, loyal customers, and stable operating cash flow. That may well be a great company.

But if the stock has already run sharply for months, turnover has expanded, and the market is already pricing in next year’s growth, the stock may no longer be especially attractive. Good numbers may produce only limited upside, while even a small disappointment in guidance or margin could trigger a colder reaction.

That is why it helps to separate facts and interpretation.

- Facts: business structure, disclosures, financials, price location

- Interpretation: how much of the good story the market already paid for

Common mistakes

- Turning business analysis into a flattering narrative without writing down the evidence

- Ignoring expectation risk because the company itself looks excellent

- Treating short-term stock strength as proof of lasting business quality

Summary

A great company and a great stock may overlap, but they are not the same question. A great company is about business quality and durability. A great stock is about whether that quality is still mispriced.

The practical order is simple: confirm whether it is a great company first, then decide whether it is a great stock at the current price.