Introduction

People often say a business has a moat, but the phrase becomes useless if it stays abstract. In practice, a moat matters only when it keeps competitors away long enough for the company to protect pricing, margins, and customer retention.

The point of this article is to turn business moat from a flattering label into a verification sequence. The real question is not whether management says the company has one. It is whether the moat shows up in numbers and customer behavior.

Why business structure matters

A moat is a defensive part of business structure. It can come from technology, brand, regulation, network effects, distribution, or customer lock-in. When that barrier is real, competitors find it harder to copy the business, and the company can usually defend profitability for longer.

That is why investors should care less about whether the market is attractive in theory and more about whether the company can hold its position without constant price cuts. A moat usually looks slower and less exciting than a growth story, but it often protects value much longer.

Core framework

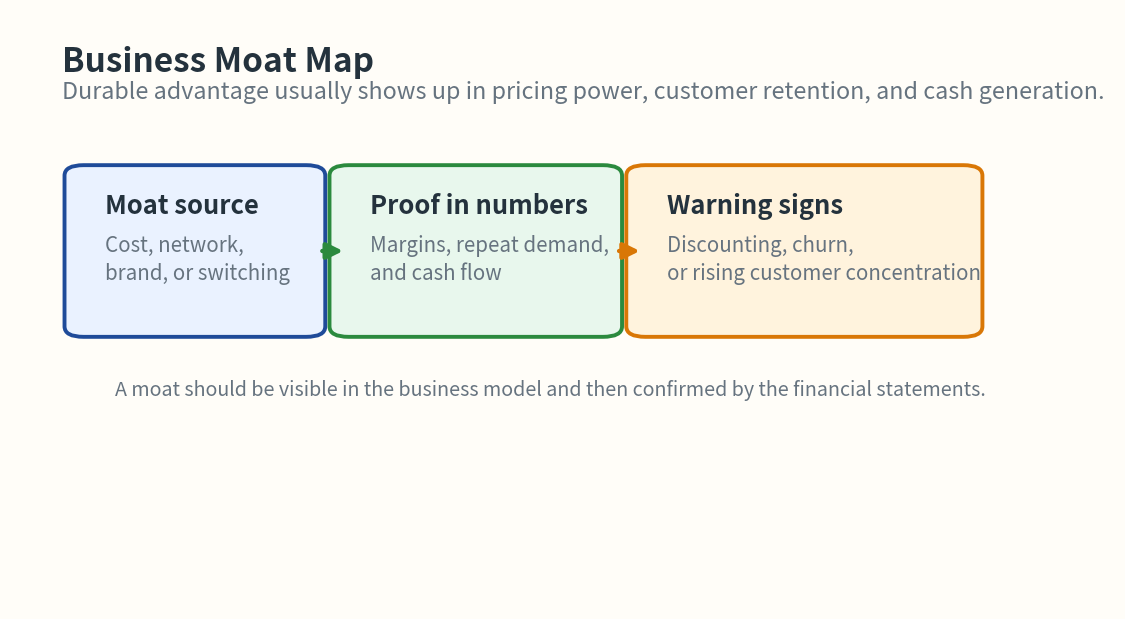

The first question is what kind of barrier exists. Technology, brand, regulation, network effects, and customer lock-in are different moats, so they require different evidence.

The second question is whether the barrier turns into pricing power and customer retention. A real moat usually leaves behind high repeat business, stable margins, and better cash generation.

The third question is whether the moat is weakening. Even a strong advantage can fade if competitors catch up, if customers become less sticky, or if the company has to rely on promotions.

Visual guide

Different moats look different, but all of them should eventually protect pricing, margins, and customer loyalty.

Where to verify it

The most practical order is:

- In the annual report, check competition, customer structure, certifications, repeat revenue, and switching costs.

- In financials, check operating margin, return profile, cash flow, and margin stability.

- In recent disclosures, check major customers, contracts, approvals, R&D, and investment support.

- In market reaction, check whether investors react more strongly to moat confirmation than to short-term noise.

The most useful sequence is type of moat -> pricing power and customer retention -> margins and cash flow -> weakening signals -> market expectations.

What to check in a company

Use this sequence:

- What is the core barrier: technology, brand, regulation, network, distribution, or customer lock-in?

- Does that barrier show up in pricing power and stable margins?

- Are repeat purchases, renewals, or switching costs actually visible?

- Are there signs that competitors are catching up?

- Has the market already priced in too much moat premium?

Investor checklist

- Did you define the type of moat instead of just repeating the word?

- Did you verify pricing power and customer retention with evidence?

- Does the moat appear in margin stability and cash generation?

- Did you check for weakening signals such as discounting or easier substitution?

- Did you separate a strong business from an already expensive stock?

Typical misunderstandings

- High market share automatically means a strong moat.

- A moat exists even if profitability does not show it.

- A moat that worked in the past will protect the company forever.

Example scenario

Imagine a software company deeply embedded in customer workflows. Switching costs are high, recurring revenue is strong, and modest price increases do not cause large customer losses. In that case, lock-in is likely functioning as a real moat.

Now imagine a manufacturer that claims technological leadership, but competitors keep launching similar products and price cuts are becoming more frequent. If margins are slipping, the moat may be weaker than the story suggests.

The practical split is:

- Facts: certifications, customer behavior, repeat revenue, margin stability, disclosures

- Interpretation: whether the moat is still protecting the business or already fading

Common mistakes

- Treating the word

moatas proof by itself - Discussing competitive advantage without connecting it to pricing power

- Ignoring signals that the barrier is getting weaker

- Assuming a great business is always a good entry point

Summary

A moat is real only if it protects pricing, margins, and customer retention for longer than competitors can easily attack. The label matters less than the evidence.

The most practical sequence is type of moat -> pricing power and customer retention -> margins and cash flow -> weakening signals -> market expectations.