Introduction

Bond ETFs are often introduced as simple income products, but their price behavior is tightly linked to interest rates and duration. That is why investors can be surprised when a bond ETF falls in price even while still paying income.

One-line summary

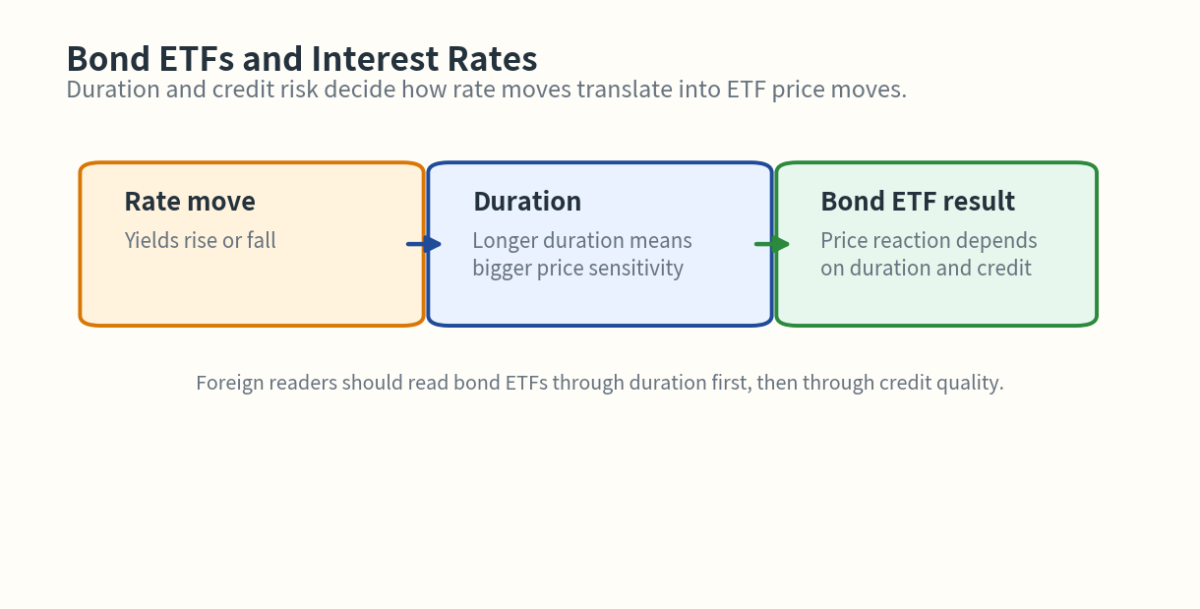

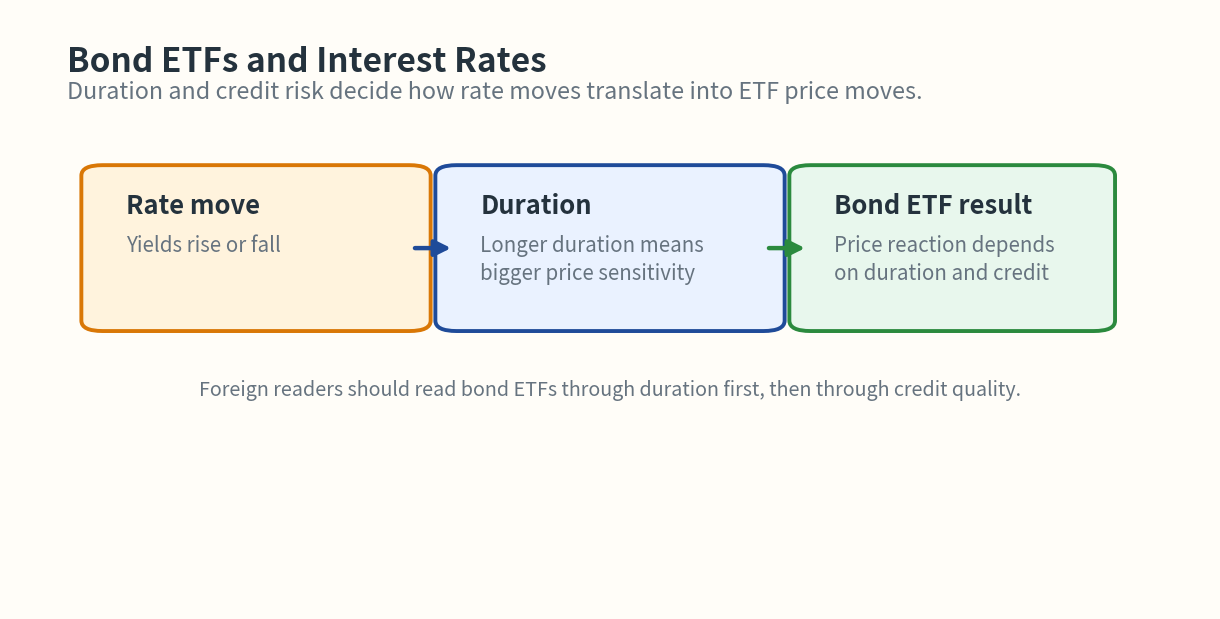

Bond ETF prices often move inversely to rates, and the size of the move depends heavily on duration.

Core framework

The cleanest split is:

- shorter-duration bond ETF: lower rate sensitivity

- longer-duration bond ETF: higher rate sensitivity

This is why investors should care not just about yield, but also about duration and which part of the rate curve matters.

Visual guide

Higher duration usually means larger price swings when rates move.

How it connects to investing

Bond ETFs can serve different jobs:

- lower volatility and cash alternative

- duration exposure

- income and allocation balance

Those roles should not be confused. A long-duration bond ETF is not the same thing as a cash-like holding.

Practical framework

Use this order:

- Check duration

- Check which yields matter most

- Decide whether the ETF role is income or rate exposure

- Ask whether current macro conditions support that role

Investor checklist

- What is the ETF’s duration?

- Which part of the yield curve matters most for it?

- Are you buying it for income or for rate sensitivity?

- Does the macro backdrop support that use?

Common mistakes

- Treating all bond ETFs as low-risk cash substitutes

- Ignoring duration

- Focusing on yield only

- Buying bond ETFs without a clear portfolio role

Summary

Bond ETFs relate to interest rates through duration. The useful framework is duration -> yield sensitivity -> portfolio role -> macro backdrop.