One-line summary

Revenue shows scale, operating profit shows the strength of the core business, and net income shows the final result after non-operating items. Investors should read all three, but operating profit and margin usually deserve the most weight first.

Why this matters

These are the three numbers that appear most often in earnings headlines. The problem is that beginners often treat them as if they mean the same thing. They do not.

Revenue tells you how much the company sold. Operating profit tells you how much money the company kept from its actual business after cost of goods sold and operating expenses. Net income adds financing items, taxes, valuation gains and losses, and one-off effects.

That means a company can report solid revenue while operating profit weakens, or stable operating profit while net income swings sharply. Good earnings reading starts by separating business structure from noise.

Where to look in DART

The most useful sources are:

company.jsonandlist.jsonfor company and filing overviewfnlttSinglAcntAll.jsonfor core financial statement accountsfnlttSinglIndx.jsonfor supporting indicators

The most practical order is:

- Revenue

- Operating profit or operating loss

- Net income or net loss

- Operating margin

- Debt ratio and ROE

This sequence lets you separate size, core profitability, final outcome, and balance-sheet burden in one pass.

Core concept

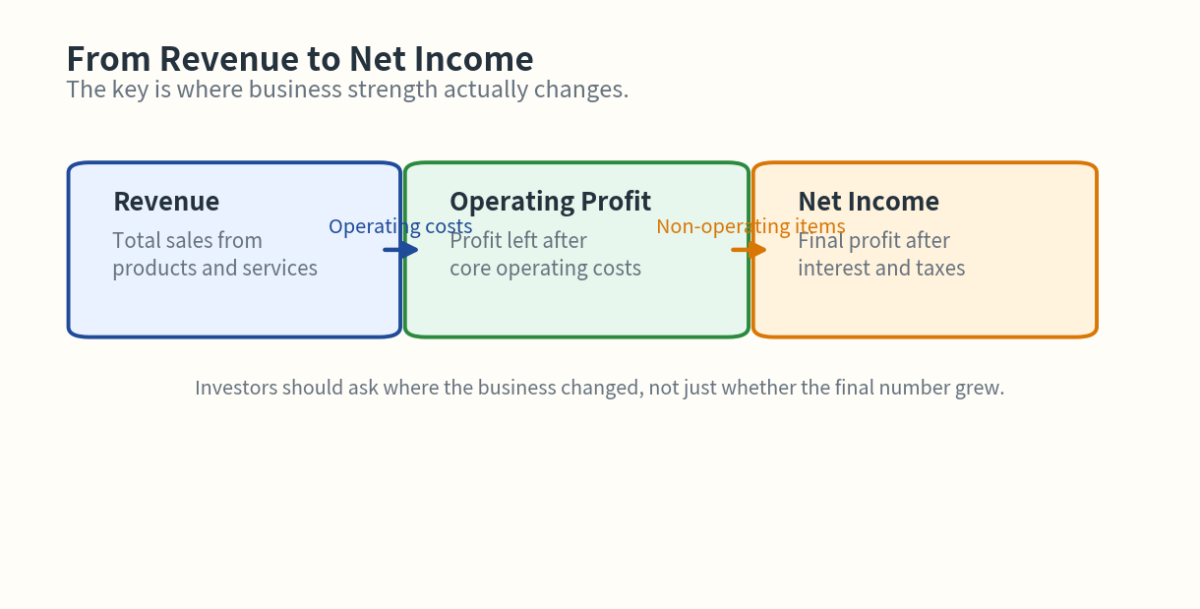

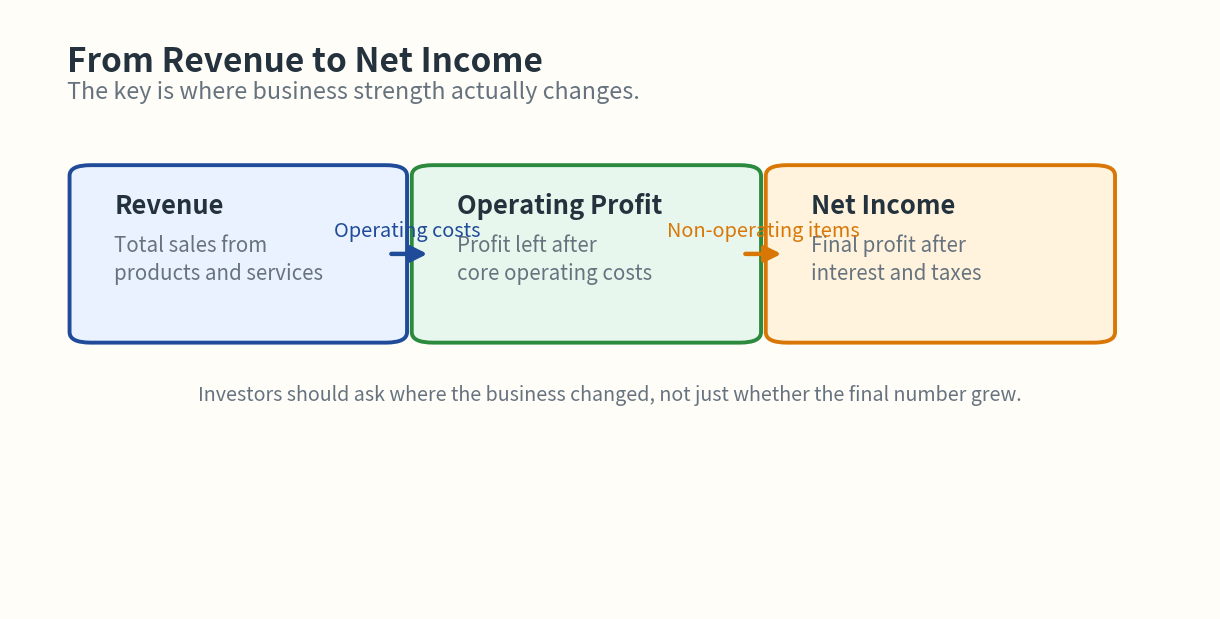

Revenue is the outermost number. It tells you about demand and scale, but not much yet about earnings quality.

Operating profit is closer to business strength. It captures pricing power, cost structure, fixed-cost leverage, and mix.

Net income is the final number, but it also carries the most noise. Interest expense, tax effects, asset sales, and other non-core items can all move it.

The practical split is:

- Revenue: scale and demand

- Operating profit: core business strength

- Net income: final result with more noise mixed in

Practical reading framework

Use this table when you open a filing:

| Number | Why it matters first | The question to ask |

|---|---|---|

| Revenue | Shows demand and scale | How much did the company sell? |

| Operating profit | Shows core business strength | How much of sales turned into profit? |

| Net income | Shows final result | Were non-core items a big factor? |

| Operating margin | Compresses earnings quality | Did economics improve, not just size? |

| Debt ratio | Shows financial burden | Can the company absorb weakness if profits slip? |

The key habit is not stopping at revenue grew. Read the next line and check whether operating profit and operating margin moved in the same direction.

Visual guide

As you move from revenue to operating profit to net income, interpretation becomes more important.

How the market reacts

Markets usually do not weigh these three numbers equally. In many cases, investors react more to:

- Operating profit and operating margin

- The quality of revenue growth

- The reason net income changed

- Whether the move looks repeatable next quarter

That is why a stock can react weakly even when revenue rises, especially if margin weakens. The reverse can also happen when revenue growth is ordinary but margin quality clearly improves.

Investor checklist

- Did revenue and operating profit move in the same direction?

- Did operating margin improve, or did only scale get bigger?

- Did net income move differently from operating profit?

- Do debt ratio and ROE support or weaken the interpretation?

- Was price reaction aligned with the numbers, or did expectations interfere?

Common mistakes

- Treating revenue growth as proof that earnings quality improved

- Treating higher net income as proof that the core business improved

- Looking at absolute profit without checking margin

- Reading balance-sheet burden separately from earnings quality

- Explaining the stock move with only one earnings line

Summary

Revenue, operating profit, and net income all matter, but they do different jobs. Revenue shows size, operating profit shows core business strength, and net income shows the final result with more noise mixed in.

The most useful habit is to separate the number that reflects structure from the number that may reflect distortion.