Introduction

The link between rates and growth stocks appears constantly in market commentary, but it only becomes useful when investors understand why it happens. Growth stocks often depend more on future cash-flow expectations than on current earnings, so a higher discount rate reduces present value more sharply.

In simple terms, when rates rise, the market tends to value money earned today more highly than profits expected far in the future.

One-line summary

Growth stocks are often more sensitive to rising rates because a larger part of their value depends on future earnings.

Key terms first

Discount rate: the rate used to convert future cash flow into today’s value.Present value: the current value of future money.Long-term yield: a longer-maturity interest rate, such as the U.S. 10-year yield.

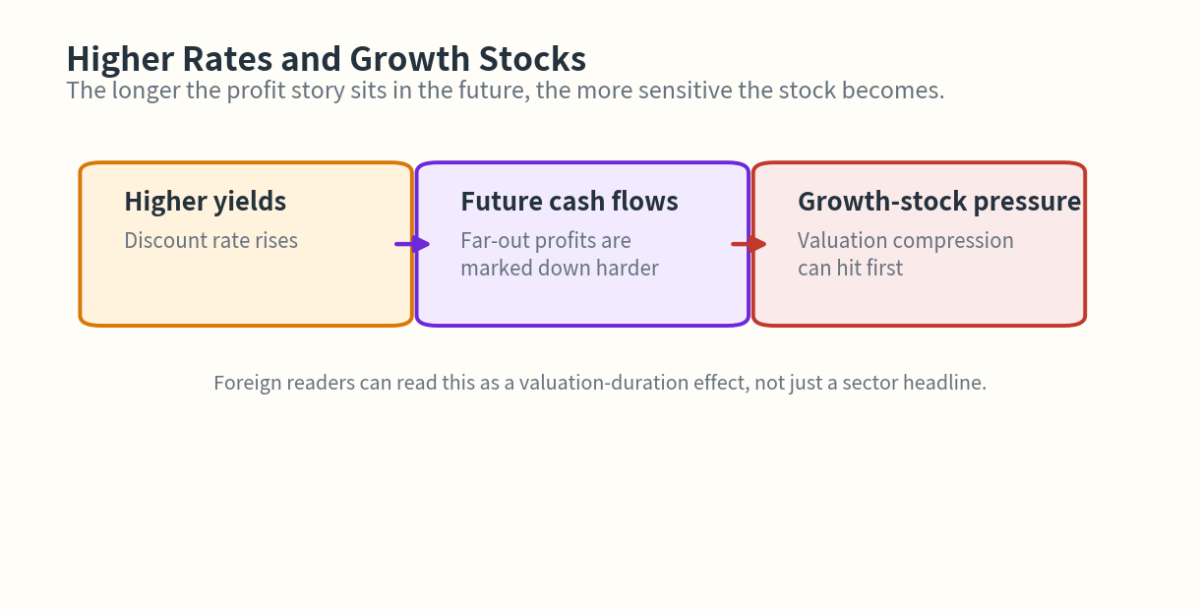

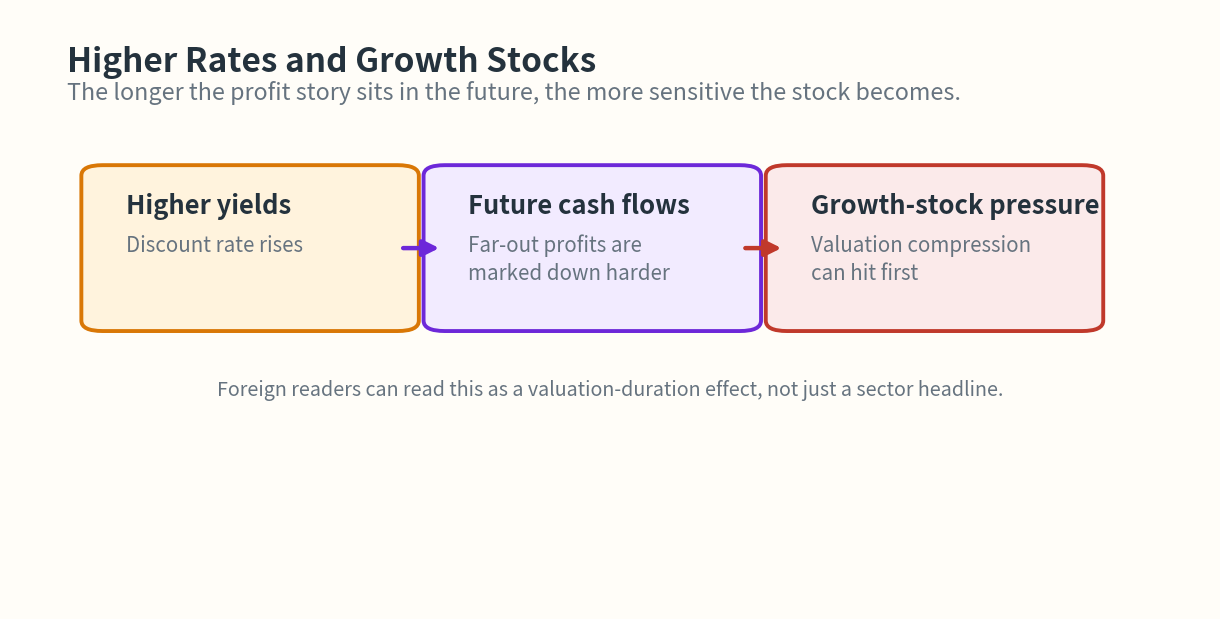

If investors expect a company’s biggest profits many years ahead, higher rates make those future profits worth less today.

Why this macro variable matters

Market yields are part of the discount rate investors use when valuing equities. When long-term yields rise, high-multiple growth stocks often feel the impact first because more of their valuation depends on distant cash flow.

The most practical chain is:

- higher long-term yields

- lower present value of distant profits

- weaker valuation support for high-duration growth stocks

How it connects to stocks

Growth stocks are often rate-sensitive for three reasons:

- more value is tied to future earnings

- valuation multiples are already high

- some growth companies still rely on external funding

By contrast, companies with current cash flow, dividends, or lower valuation dependence on distant growth often react less violently.

Visual guide

For growth stocks, the discount rate can matter almost as much as the earnings line itself.

Real data example

The 2022 to 2023 rate shock is the most useful reference period. The U.S. 10-year Treasury yield moved from roughly 1.5% at the end of 2021 to nearly 5% at one point in 2023. During that stretch, markets repeatedly repriced long-duration growth stocks.

| Real period | What happened in markets | Reading point |

|---|---|---|

| 2022 rate surge | High-P/E tech and unprofitable growth sold off hard | Discount-rate pressure hit valuation first |

| Second half of 2023 | Even large-cap tech became more volatile as long yields jumped | Good earnings do not fully erase short-term rate pressure |

Not every growth stock fell by the same amount. Areas such as AI and semiconductors could resist part of the pressure when earnings revisions were accelerating quickly. The practical lesson is rates + earnings revisions, not rates alone.

How investors can use it

The practical question is not Are rates high? but Which part of the market still relies on distant profits?

- Check the 10-year yield and real yields first.

- Separate profitable large-cap compounders from cash-burning speculative growth.

- Look for earnings revisions strong enough to offset valuation pressure.

- In Korea, watch whether the pressure shows up first in

KOSDAQ, South Korea’s growth-heavy junior market, before it spreads to largerKOSPInames.

Practical framework

Use this order:

- Check the long-term yield direction

- Check whether real yields are rising too

- Separate profitable large-cap growth from cash-burning speculative growth

- Ask whether earnings revisions are strong enough to offset the rate pressure

What to watch together

- Watch the

10-year U.S. Treasury yield, not only central-bank policy headlines. The valuation pressure usually arrives through market yields first. - For Korean investors, the spillover often shows up through

KOSDAQ, internet stocks, secondary-battery names, and other longer-duration equity stories before it shows up in more defensive value segments.KOSDAQis South Korea’s more growth-oriented junior market. - If real yields are rising while earnings revisions are flat, the setup is usually harder for growth than when yields rise alongside sharply improving profit expectations.

Investor checklist

- Is the 10-year yield rising or falling?

- Are real yields rising too?

- Is the stock dependent on distant growth rather than current cash flow?

- Are earnings revisions strong enough to offset the valuation pressure?

- Is the company exposed to refinancing or funding risk?

Common mistakes

- Treating all growth stocks as equally rate-sensitive

- Watching policy rates but ignoring market yields

- Ignoring earnings revisions

- Treating valuation pressure as the same thing as business weakness

Summary

Rising rates pressure growth stocks because future earnings lose value when discounted at a higher rate. The best way to read the setup is yield direction -> real yields -> earnings revisions -> funding structure.